Beyond Push: A Pull-Based Model For Comparator Supply

By John O’Brien

Part 2 of a four-part series: “Beyond Bulk — Rethinking Comparator Supply for Modern Clinical Trials”

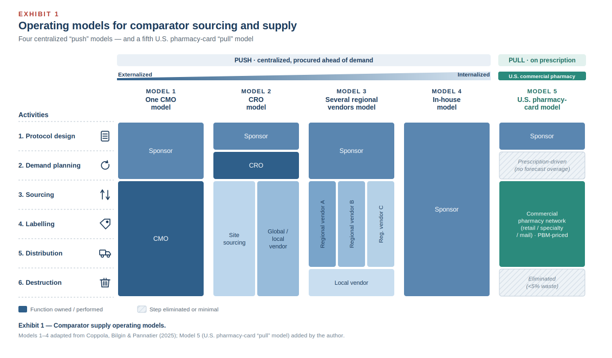

In the first article of this series, I argued that comparator sourcing is one of the most underappreciated risks in clinical trial operations — an expensive afterthought owned by no single function and governed by a conventional “push” logic that forces sponsors to procure in bulk, label, warehouse, and distribute product months before a patient ever enrolls. That logic is the common thread running through every model the industry currently recognizes. The four centralized models Coppola, Bilgin, and Pannatier laid out last year — CMO-led, CRO-led, regional vendor, and in-house — differ in who performs each step, but all four assume the sponsor buys ahead of demand and ships toward the patient.¹

I closed the first article by promising a different approach: an on-demand, just-in-time, prescription-based “pull” model, available in the United States, that can cut comparator lead times by roughly 75%, hold waste under 5%, and unlock cost levers the push model structurally cannot reach. This article takes up the first half of that promise — what the model is, how it works, and how product reaches the patient. The next turns to where it fits, where it breaks down, and what it actually costs.

What The Pull Model Actually Is

In a push model, the unit of planning is the forecast. You estimate enrollment, apply a country activation curve and a screen failure assumption, add an overage buffer, and procure against that projection — long before the first patient signs a consent form. In a pull model, the unit of planning is the prescription. Nothing moves — and no product dollars are committed — until a patient is enrolled and a clinician writes an order.

Mechanically, the sponsor partners with a vendor that sits on top of the existing U.S. commercial pharmacy infrastructure rather than building a parallel clinical supply chain. The comparator is dispensed as a prescription through a commercial retail or specialty pharmacy network, paid for at the point of dispensing via a study-specific prescription card — running on the same back-end “insurance rails” that adjudicate a normal retail pharmacy claim, repurposed for trial supply.² Because these vendors aggregate volume across many programs, they negotiate pricing through pharmacy benefit managers (PBMs) rather than paying a one-off clinical supply premium.

Standing the model up is a four-step exercise rather than a nine-month procurement campaign:

- Contracting and strategy — Supply agreements, scope, and the comparator strategy itself (which products, which sites, which strengths) are developed.

- Vendor configuration — This includes platform setup, prescription templates for mail-order and specialty pharmacies, and the study-specific dispensing card. Functionally, the card behaves like a commercial insurance or co-pay card: it tells the pharmacy how to adjudicate and bill the fill to the sponsor’s program. Some vendors issue these cards fully electronically and instantly; others still physically mail printed cards to sites for patients to use, which adds days and a logistics step worth asking about up front.

- Network configuration — The program is mapped to the appropriate PBM and pharmacy network.

- Launch — The card goes live, and dispensing begins on demand.

The headline effect is on time. A traditional comparator can take nine to 15 months³ to move from procurement through clinical labeling, GMP warehousing, and site distribution. A pharmacy card program can be live in as little as 30 days, because the product is already sitting on commercial shelves — fully approved, labeled, and in date. That is the source of the 75% lead time reduction, and it is also where the waste story begins: you cannot expire inventory you never bought.

Importantly, this does not remove operational responsibility from the sponsor; it shifts control out of procurement and distribution infrastructure and into pharmacy-network configuration, where oversight still depends on defined study-level governance and site capability alignment. The model changes where the work lives, not whether it has to be done.

Getting Product To The Patient: White-Bagging Vs. Direct-To-Patient

A pharmacy card model has two delivery endpoints, and the choice has both operational and legal dimensions.

White-bagging — The pharmacy ships the dispensed product to the trial site for administration. Sites do not universally love it, but in a research context the usual objection evaporates: there is no financial conflict, because the site is no longer buying and marking up the drug. It is worth addressing the legal question head-on, because it comes up. As of mid-2025, roughly a dozen states had enacted restrictions on mandatory white-bagging and brown-bagging.⁴ But read what those laws actually target: they prohibit payers and PBMs from forcing a patient or provider to use a payer-selected pharmacy as a condition of insurance reimbursement or coverage.⁵ That triggering mechanism is absent in sponsor-funded research. There is no payer mandate, no reimbursement condition, and no revenue motive — the sponsor is funding the comparator, exactly as it would under the bulk model, not steering a covered claim. The state white-bagging statutes, on their plain terms, do not reach the research supply use case.

Direct-to-patient (DtP) — The pharmacy ships to the patient’s home. This aligns the model with the broader decentralized trial movement, and it materially improves access for patients who live far from a major trial site. It also introduces chain of custody and cold chain considerations that have to be designed in, not assumed. For the right comparator and the right protocol, DtP turns a sourcing decision into a patient centricity advantage.

In-person pickup — For an oral self-administered comparator (the model’s most common use case), the simplest path is the patient collecting the prescription at the dispensing pharmacy, exactly as they would any retail script. A terminology note, since it causes confusion: the various “bagging” practices — brown, clear, and gold — describe how a provider-administered specialty drug is routed for administration, not how a patient picks up an oral medication, and are largely tangential here. Brown-bagging in particular (the patient carrying the drug to the clinic) is frequently barred by health systems and rarely fits a trial.

The pharmacy card model offers a fundamentally different approach to comparator sourcing, replacing forecast-driven inventory strategies with dispensing tied directly to patient enrollment and demand. As with any supply model, however, operational feasibility is only part of the equation. Sponsors must also understand where the model fits, how it affects total cost of ownership, inventory exposure, and waste, as well as how much control it hands back over comparator spend. Those questions — and the economics behind them — are the subject of the next article.

Acknowledgments. Special thanks to Toni-Joy Motomura and Brian Horan for their review and editorial input in shaping this article.

References

- Coppola G, Bilgin P, Pannatier S. 4 centralized comparator sourcing models to fortify supply chains. Clinical Supply Leader. July 15, 2025.

- SupplyRx, Inc. Cloud-based pharmacy card platform for open-label clinical trial supply. https://www.supplyrx.com. Accessed June 2026.

- International Society for Pharmaceutical Engineering. ISPE Good Practice Guide: Comparator Management. ISPE; 2012. (Sourcing-to-distribution lead times.)

- American Medical Association / American Society of Clinical Oncology. Mandatory White Bagging and Brown Bagging Policies Threaten Patient Access to Care (issue brief). July 2025.

- Avalere Health. White-bagging legislation gains popularity in state legislatures. 2025–2026.

About The Author:

John O’Brien is a clinical supply chain professional with experience managing comparator sourcing and distribution for global oncology clinical trials. His 2022 master’s capstone (CCP)project focused on re-engineering comparator supply through commercial pharmacy network integration and insurance cost-sharing, including collaboration with researchers at the Tufts Center for the Study of Drug Development, BeiGene (now BeOne Medicines), Myonex, TrialCard (now Veralis), and SupplyRx. This is the second article in a four-part series for Clinical Supply Leader.

John O’Brien is a clinical supply chain professional with experience managing comparator sourcing and distribution for global oncology clinical trials. His 2022 master’s capstone (CCP)project focused on re-engineering comparator supply through commercial pharmacy network integration and insurance cost-sharing, including collaboration with researchers at the Tufts Center for the Study of Drug Development, BeiGene (now BeOne Medicines), Myonex, TrialCard (now Veralis), and SupplyRx. This is the second article in a four-part series for Clinical Supply Leader.