R&D Capitalization Decisions That Drive Clinical Trial Supply

By Amanda Laskey, life sciences senior analyst with RSM US LLP

As life sciences companies prepare for upcoming tax filings, decisions regarding the capitalization of research costs are increasingly intersecting with operational and cash-flow planning, including clinical supply strategy. For clinical supply teams managing inventory commitments and planning supply chain strategies, decisions around Sec. 174/174A capitalization can directly influence how much capital is available to support trial execution.

Research Capitalization Changes Create Flexibility For Future Strategies

For life sciences companies that have been statutorily required to capitalize domestic research and experimental (R&E) expenditures under Sec. 174 for the past few years, there are several levers to pull that can impact potential cash tax savings. These options allow companies to better align their tax strategy with broader business priorities, including supply operations, budgeting, and commercialization strategies.

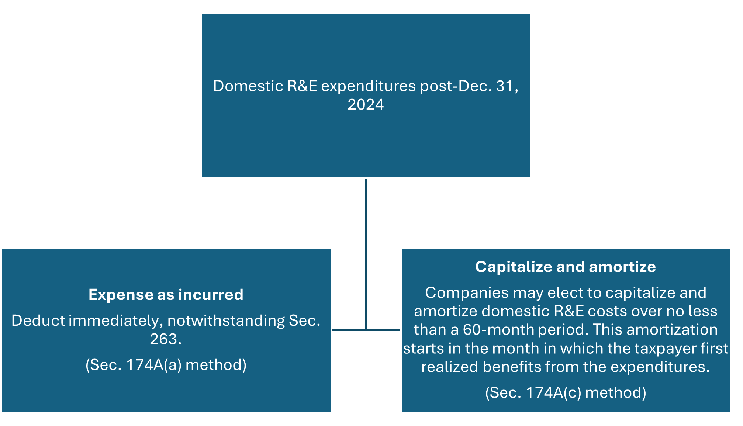

Under new tax provisions enacted through the One Big Beautiful Bill Act (OBBBA), companies have two options for how to treat domestic research expenditures incurred in tax years beginning after Dec. 31, 2024.

In addition, a taxpayer who elects to expense domestic R&E costs as incurred may continue to capitalize domestic research expenditures and amortize them over a 10-year period under Sec. 59(e), which is an annual election available to taxpayers versus an accounting method. This decision is separate from the decision to expense costs as incurred under Sec. 174A(a) or to capitalize and amortize under Sec. 174A(c), which should be made on an accounting method change filed with a company’s Dec. 31, 2025 tax return.

For flow-through entities, this election is made at the investor level rather than the entity level, again showing that this can be done as a viable tax planning tool regardless of the overall accounting method of the entity incurring Sec. 174 costs.

Clinical supply leaders planning trials may want to evaluate the impact on how the capitalization strategy may align, or diverge, from overall clinical strategy. Precommercial companies solely conducting trials may choose to delay deductions for a future period in which they can receive the associated benefits.

Aligning Treatment Of Unamortized Domestic Costs With Trial And Business Strategy

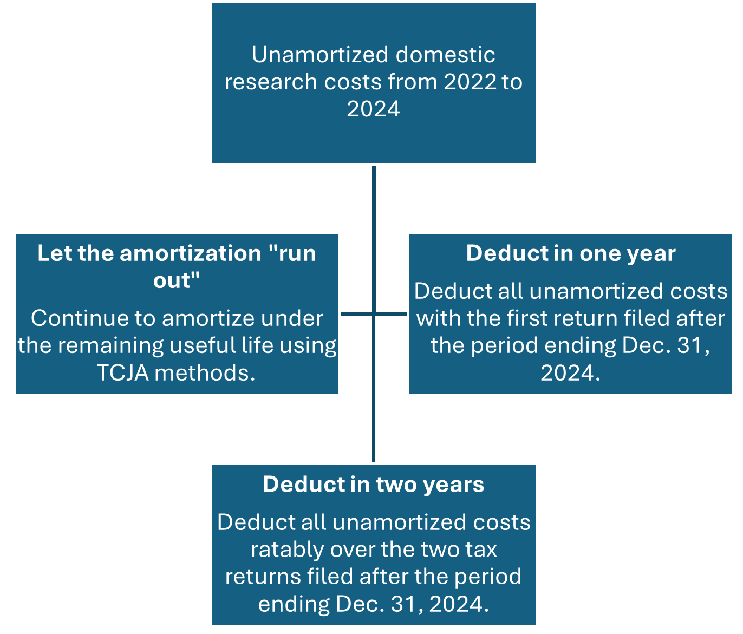

While only small businesses are permitted to amend earlier returns to retroactively apply the changes regarding domestic research expenditures, the OBBBA provides an election for all taxpayers to accelerate and deduct in the current year any remaining unamortized domestic research expenditures that were incurred in tax years 2022 to 2024. Life sciences companies have three options regarding their unamortized domestic costs from 2022 to 2024:

The key aspect relating to the domestic R&E capitalization changes is that there is immense flexibility. When deciding on the treatment of historic unamortized domestic R&E costs, companies should be looking toward their overall business goals, administrative capacity, and broader tax strategy. For example, for a company expecting to license a molecule in 2026 to fund a Phase 2 trial on another product, it may make sense to deduct all unamortized costs ratably over the tax years ending Dec. 31, 2025 and Dec. 31, 2026.

For companies with expected tax cash outlays for the 2025 tax year, it may make sense to deduct all unamortized domestic costs in 2025, freeing cash for accelerated manufacturing or other trial costs. For precommercial companies with little to no expected tax cash payments in 2025 and 2026, continuing to let the 2022 to 2024 costs amortize over the remaining useful life may be the best option to support longer, capital-constrained trials.

Federal Tax Treatment Doesn’t Always Align With State Rules Or Capacity

Companies should also evaluate whether any states in which they file do not conform with the new federal treatment and require continued capitalization of domestic research and development costs. If a taxpayer has a material filing position in these states, continued tracking regarding Sec. 174 costs may still be required, adding a tax compliance burden that, on the surface, should have been alleviated with the passage of OBBBA.

As the Sec. 174A(c) method requires project-by-project tracking of costs and only allows for amortization to begin in the month in which the taxpayer first realized benefits from such expenditures, companies may not have the administrative capacity to continue to capitalize domestic Sec. 174A costs. Frequently, clinical supply costs are not tracked on a project-by-project basis, so the administrative challenges associated with capitalizing under Sec. 174A(c) may fall onto the clinical supply team. Involving clinical supply leadership in modeling discussions can help ensure that tax strategies align with trial strategy, anticipated phase transitions, and bookkeeping requirements.

Clinical Supply Leaders Are Crucial In The Capitalization Process

Foreign research and experimental expenditures still require capitalization and amortization ratably over a 15-year period, beginning with the midpoint of the year in which the costs are paid or incurred. Clinical supply leaders may need to assist with investigating which vendors are performing work outside of the United States, Puerto Rico, or any U.S. possession.

Furthermore, the clinical team plays a crucial role in determining where research supplies are used or consumed. Sometimes a clinical lot is manufactured in Europe using an active pharmaceutical ingredient produced in Asia, then shipped to 75 different trial locations around the world. Understanding the complex supply chains relating to clinical trials is of crucial importance in determining the appropriate treatment of these costs.

The Takeaway

Sec. 174/174A changes introduce meaningful flexibility, but the impact on clinical trial supply is highly dependent on how tax elections align with trial timelines and manufacturing commitments. Clinical supply leaders should be actively involved in these decisions to ensure tax strategy supports trial execution and capital allocation.

About The Author:

Amanda Laskey is a senior manager in the tax services practice in the New York City office of RSM US LLP, focusing on clients within the life sciences industry. In addition, she is a member of the firm’s Industry Eminence Program and works alongside RSM’s chief economist and other senior analysts to understand, forecast and communicate economic, business and technology trends affecting middle market businesses.

Amanda Laskey is a senior manager in the tax services practice in the New York City office of RSM US LLP, focusing on clients within the life sciences industry. In addition, she is a member of the firm’s Industry Eminence Program and works alongside RSM’s chief economist and other senior analysts to understand, forecast and communicate economic, business and technology trends affecting middle market businesses.